Modern Auditing: Assurance Services And The Integrity Of Financial Reporting 8E

基本信息

Format:Hardback 1056 pages

Publisher:John Wiley & Sons Inc

Imprint:John Wiley & Sons Inc

Edition:8th Edition

ISBN:9780471230113

Published:5 Aug 2005

Classifications:Management accounting & bookkeeping

Readership:Professional & Vocational

Weight:1900g

Dimensions:260 x 208 x 41(mm)

頁面參數僅供參考,具體以實物為準

書籍簡介

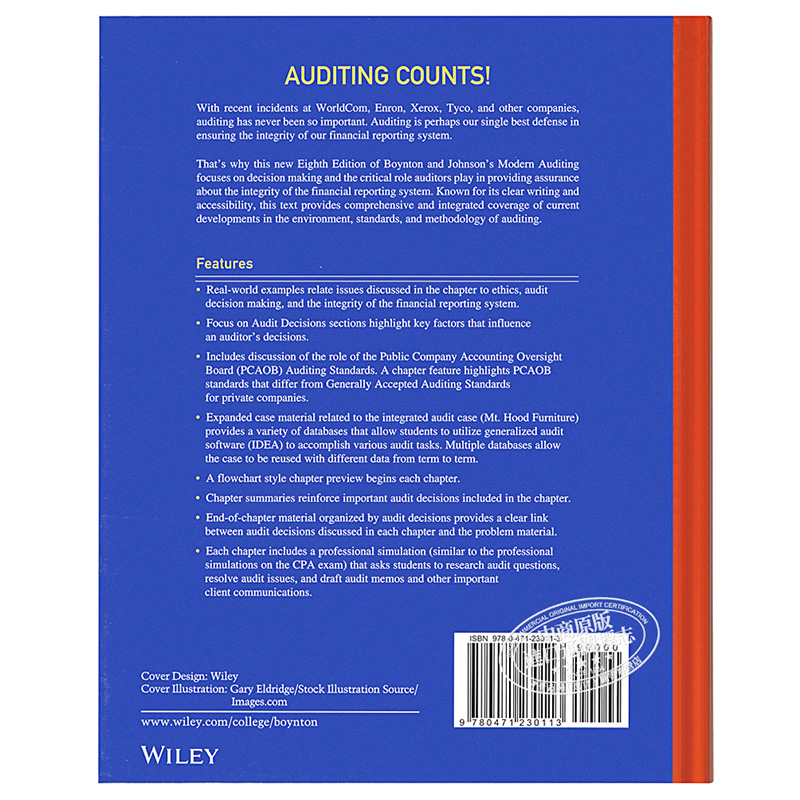

Known in the academic market for its clear writing style and accessibility, this extensive revision focuses on auditor decision making and the auditor?s role in providing assurance about the integrity of the financial reporting system. This is particularly important in light of the recent events involving WorldCom, Enron, Xerox, Aldelphia, Tyco, Waste Management, and other recent incidents that have questioned the quality of work in the auditing profession. Intended for a junior- or senior-level course in auditing or assurance services taught at most four-year schools.

NEW TO THIS EDITION

Chapter Opening Vignette uses real world examples to relate issues discussed in the chapter to ethics, audit decision-making and the integrity of the finanancial reporting system

Chapter feature titled, ‘Focus on Audit Decisions’ highlights key factors that influence an auditor’s decisions

The book includes discussion of the role of the Public Company Accounting Oversight Board (PCAOB), PCAOB Auditing Standards and a chapter feature will highlight PCAOB standards that differ from Generally Accepted Auditing Standards for private companies

Expanded case material related to the integrated audit case, ‘Mt. Hood Furniture’ case provides a variety of databases that allow students to utilize generalized audit software (IDEA) to accomplish various audit tasks. Multiple databases allow the case to be re-used with different data from term to term.

Flowchart style chapter preview at commencement of each chapter

Chapter summaries reinforce important audit decisions included in the chapter. They will (1) identify the audit decisions discussed in the chapter and provide page references to detailed discussions that (2) identify the factors that influence the auditor’s decision, and (3) explain the audit decision.

End of chapter material organized by audit decisions so that there is a clear link between audit decisions discussed in each chapter and the problem material

Professional simulations for each chapter that provide a more comprehensive problem that addresses the type of professional simulation problems that students will encounter on the the CPA Exam. This is supported with additional on-line simulations.

目錄

PART 1: THE AUDITING ENVIRONMENT.

1. Auditing and the Public Accounting Profession-Integrity of Financial Reporting.

2. Auditors' Responsibilities and Reports.

3. Professional Ethics.

4. Auditor's Legal Liability.

PART 2: THE DECISION MAKING OF AUDIT PLANNING.

5. Overview of the Financial Statement Audit.

6. Audit Evidence.

7. Accepting the Engagement and Planning the Audit.

8. Materiality Decisions and Performing Analytical Procedures.

9. Audit Risk: Including the Risk of Fraud.

10. Understanding Internal Control .

PART 3: THE DECISION MAKING OF COLLECTING AND EVALUATING EVIDENCE.

11. Audit Procedures in Response to Assessed Risks: Tests of Controls.

12. Audit Procedures in Response to Assessed Risks: Substantive Tests.

13. Audit Sampling.

PART 4: AUDITING THE TRANSACTION CYCLES AND COMPLETING THE AUDIT.

14. Auditing the Revenue Cycle.

15. Auditing the Expenditure Cycle.

16. Auditing the Production and Personnel Services Cycles.

17. Auditing the Investing and Financing Cycles.

18. Auditing Investments and Cash Balances.

19. Completing the Audit / Post Audit Responsibilities.

PART 5: OTHER ATTEST AND ASSURANCE SERVICES.

20. Attest and Assurance Services, and Related Reports.

21. Internal, Operational, and Governmental Auditing .

Index.

作者簡介

William C. Boynton, Ph.D., CPA received his doctorate in accounting from Michigan State University. He is professor emeritus of accounting at California Polytechnic State University at San Luis Obispo where he formerly served as dean and head of the Accounting Department. He has served on the audit staffs of two international public accounting firms. He has also served as a regional chairperson of the Auditing Section of the American Accounting Association, and on a variety of committees for the American Accounting Association and the Federation of Schools of Accountancy. He is the author or coauthor of several articles and committee reports on accounting and auditing, and has served as codirector of the American Institute of Certified Public Accountants, he has served on its Globalization Task Force and its Committees on Accounting Education, the 150-Hour Requirement, and Accounting Principles and Auditing Standards. He is a recipient of the California Society of Certified public Accountants Faculty Excellence Award.

Raymond N. Johnson, Ph.D., CPA received his doctorate in accounting from the University of Oregon. He is a professor of accounting at Portland State University where he formerly served as head of the Accounting Department, Assistant to the Vice President for Finance and Administration and Assistant to the Provost. He has served on the audit staffs of two international public accounting firms and one local firm. He also served as a consultant to the Auditing Standards Board and was a member of the AICPA Control Risk Audit Guide Task Force. Dr. Johnson currently is a member of the Oregon Board of Accountancy and he is a Past-President of the Oregon Society of CPAs, a former member of AICPA Council (the AICPA's governing body). He led successful legislative and regulatory initiatives in Oregon to expand the pathways to earn the CPA designation. In addition, he has been an American Council on Education Fellow and an Arthur Young McClelland Moores Post-Doctoral Fellow. Dr. Johnson is the recipient of a Leadership Award from the Oregon Entrepreneurs Forum and the Earl Wantland Outstanding Business Professor at Portland State University.

評論曬單